Olahraga

Lihat Semua →

Arsenal Dikabarkan Buka Pembicaraan Bruno Guimaraes, Newcastle Tegaskan Belum Ada Penawaran

Newcastle United menegaskan belum menerima penawaran resmi atau kontak langsung dari Arsenal terkait transfer gelandang ...

Arsenal Incar Bruno Guimaraes, Tawaran Hamburg untuk Vieira Membalas

Arsenal terus memperkuat skuadnya di bursa transfer musim panas 2026 dengan menargetkan gelandang Newcastle United, Brun...

Arsenal Incar Penyerang Leipzig Yan Diomande, Pengganti Morgan Rogers

Arsenal dilaporkan telah mengajukan pertanyaan resmi terkait kondisi transfer penyerang RB Leipzig, Yan Diomande. Langka...

Parlemen Prancis Sahkan UU Reformasi Sepak Bola, Pangkas Kesenjangan Ligue 1

Parlemen Prancis resmi mengesahkan undang-undang reformasi sepak bola profesional guna mengatasi krisis ekonomi dan tata...

Vicario Absen Tur Pramusim Tottenham, Sinyal Musim Depan ke Serie A

Kiper Tottenham Hotspur Guglielmo Vicario tidak diikutsertakan dalam skuad tur pramusim ke Selandia Baru karena mengalam...

Ekonomi

Lihat Semua →

NPR Kembali Gelar Planet Money Summer School, Angkat Gagasan Ekonomi Dunia

Media ternama NPR kembali meluncurkan program podcast unggulannya, Planet Money Summer School. Musim terbaru ini membeda...

Trump Berlakukan Tarif 50% untuk Barang Kanada, Memicu Ancam Perang Dagang

Presiden AS Donald Trump resmi memberlakukan tarif impor sebesar 50% pada sebagian besar produk asal Kanada dengan tuduh...

AS Disebut Bakal Kembalikan Status Dagang Spesial Hong Kong, Sinyal Hubungan Membaik dengan China

Kementerian Perdagangan China memberikan sinyal bahwa Amerika Serikat (AS) akan memulihkan hak istimewa perdagangan bagi...

Garuda Indonesia Ubah Aturan Bagasi Gratis, Kini Dihitung per Koper

PT Garuda Indonesia (Persero) Tbk akan mengubah skema jatah bagasi gratis untuk seluruh penumpang dari sistem berat tota...

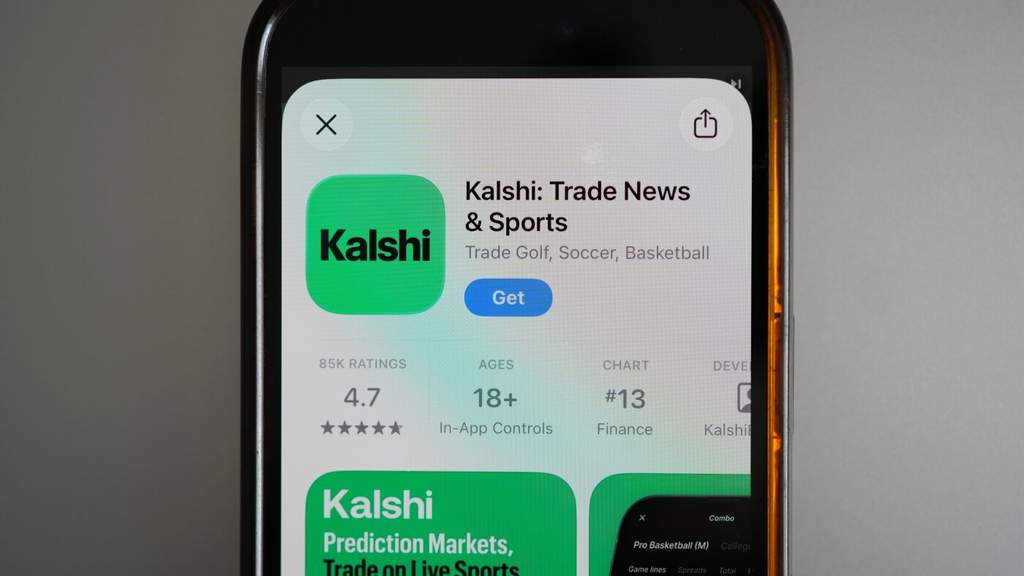

Taruhan Piala Dunia Melonjak, Kalshi Bantah Disebut Rumah Judi Olahraga

Platform pasar prediksi Kalshi mencatatkan lonjakan transaksi taruhan Piala Dunia hingga mencapai USD 40 miliar, jauh me...

Teknologi

Lihat Semua →

New York Times Tuding Gedung Putih Penyalahgunaan Hukum, Intimidasi Wartawan

Surat kabar harian asal Amerika Serikat, The New York Times (NYT), berhadapan dengan Departemen Kehakiman AS di pengadil...

AI Rilis 10 Universitas Paling Berpengaruh di Jakarta, Paramadina Masuk Daftar

Kecerdasan buatan (AI) melalui ChatGPT merilis daftar 10 universitas di Jakarta yang dinilai paling berpengaruh dan bany...

Mainan AI Ancam Tumbuh Kembang Anak, Pakar Ingatkan Risiko 'Trojan Teddy Bear'

Gelombang adopsi kecerdasan buatan (AI) kini mulai merambah ke dunia mainan anak-anak dengan wujud boneka dan robot pint...

Biaya Membengkak, Startup AS Mulai Beralih ke Model AI Murah Asal China

Biaya operasional kecerdasan buatan (AI) yang kian melonjak memaksa sejumlah startup di Amerika Serikat mengambil langka...

Fosil T-Rex Bernama Gus Terjual Rp 813 Miliar, Tuai Protes Ilmuwan

Fosil Tyrannosaurus rex sepanjang 38 kaki bernama Gus memecahkan rekor dunia setelah terjual seharga 50,1 juta dolar AS ...